The final Jacksonville City Council vote on Jacksonville Mayor Lenny Curry‘s pension reform bills is still a few days a way.

However, the “Committee of the Whole” meeting to be held Wednesday afternoon stands as an excellent preview of what is to come — a closing argument.

The Curry team — especially the political side — would hold that everyone on the council should, in fact, vote in the affirmative … and that vote should happen in the committee of the whole.

There is no obligation to vote Wednesday, though a vote can be taken if the council is comfortable.

Curry’s political team believes that comfort level should have been reached.

Privately, they have wondered why it is that more council members aren’t rushing to endorse the pension reform solution.

They have committed a six-figure budget to ads in heavy rotation on television.

As well, they have commissioned an internal poll, one which shows the mayor with 70 percent approval and pension reform at 71 percent.

A subtext of the poll: the relative popularity of the Jacksonville City Council is yoked to the charismatic mayor and his reform agenda.

The game being played: political hardball.

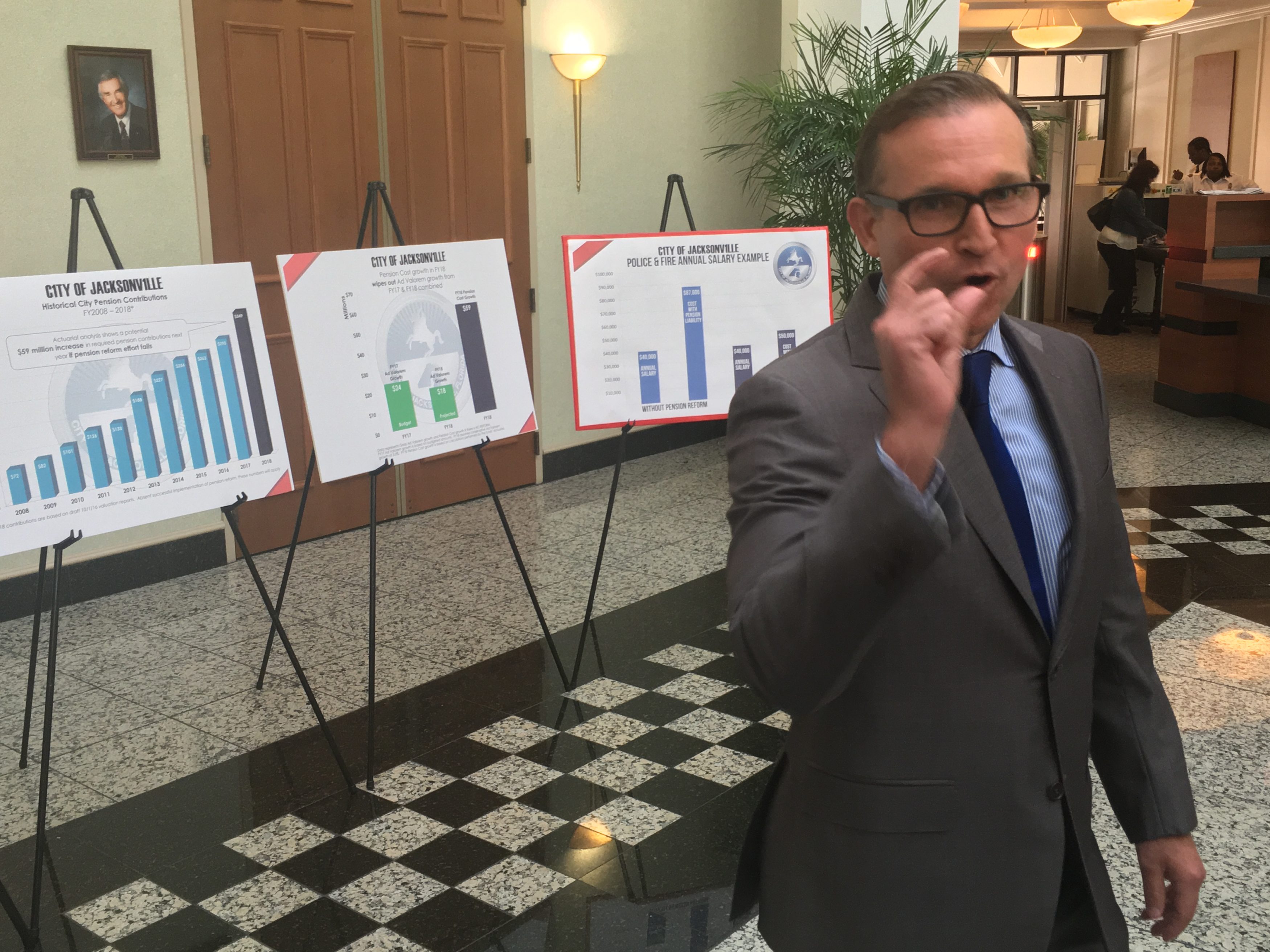

The political stakes are high for all parties: without immediate pension reform, costs of the unfunded actuarial liability on the city’s $2.8B pension debt will be $360M next year — out of a general fund budget that is barely three times that number.

Such a hit would be political suicide for the current leadership class.

Curry’s pension reform has its critics, and his team isn’t selling the legislation as perfect — but as the most palatable of a menu of bad options.

His team will want to see a vote. And will want it to be 19-0.

Will that happen?

___

Three of the 14 filed bills are probably the most important: 2017-257 creates a new ordinance section: Chapter 776 (Pension Liability Surtax).

Bill 2017-258 affects the general employees and correctional worker plans, closing the extant defined benefit plans to those hired after Oct. 1, 2017, and committing the city to a 12 percent contribution for those general employees and a 25 percent contribution for correctional officers hired after October.

Bill 2017-259 implements revisions to the Police and Fire & Rescue plans.

258 and 259 both offer fixed costs via a defined contribution plan for new hires, while offering generous contributions from the city to those hires, and raises for all current employees.

The best deals are for public safety: long-delayed raises to current employees (a 3 percent lump sum payout immediately, and a 20 percent raise for police and fire over three years) and gives all classes of current employees the same benefits.

As well, all police and fire officers will have DROP eligibility with an 8.4 percent annual rate of return and a 3 percent COLA.

The deal, if approved without modification, will bring labor peace through 2027 — though it can be renegotiated by the city or the unions at 3, 6, 9, and 10 years marks in the agreement.

For new employees, however, the plan is historic — a defined contribution plan that vests three years after the new employee for police and fire is hired.

The total contribution: 35 percent, with the city ponying up 25 percent of that — with guarantees that survivors’ benefits and disability benefits would be the same for new hires as the current force of safety officers.

The Curry model, rooted in a deferred contribution approach that increases a re-amortized liability and spreads out costs to hit hardest when the sales tax extension money starts coming in after 2030, is intended to provide fixed costs and certainty for budgets.