The real work was done over the past weeks and months. But the ceremony, the cameras, the victory lap were all reserved for Monday afternoon, when the Jacksonville City Council officially passed 14 bills that equate to pension reform.

The “committee of the whole” vote – held Wednesday – was the dispositive one.

In that meeting, which lasted over three hours, the Jacksonville City Council worked through the last few rounds of questions and concerns it might have had over the pension agreements.

Those questions and concerns, really, were moot points.

The city can’t afford not to make the deal – not facing an untenable $360M pension hit next year on a $2.8B unfunded actuarial liability.

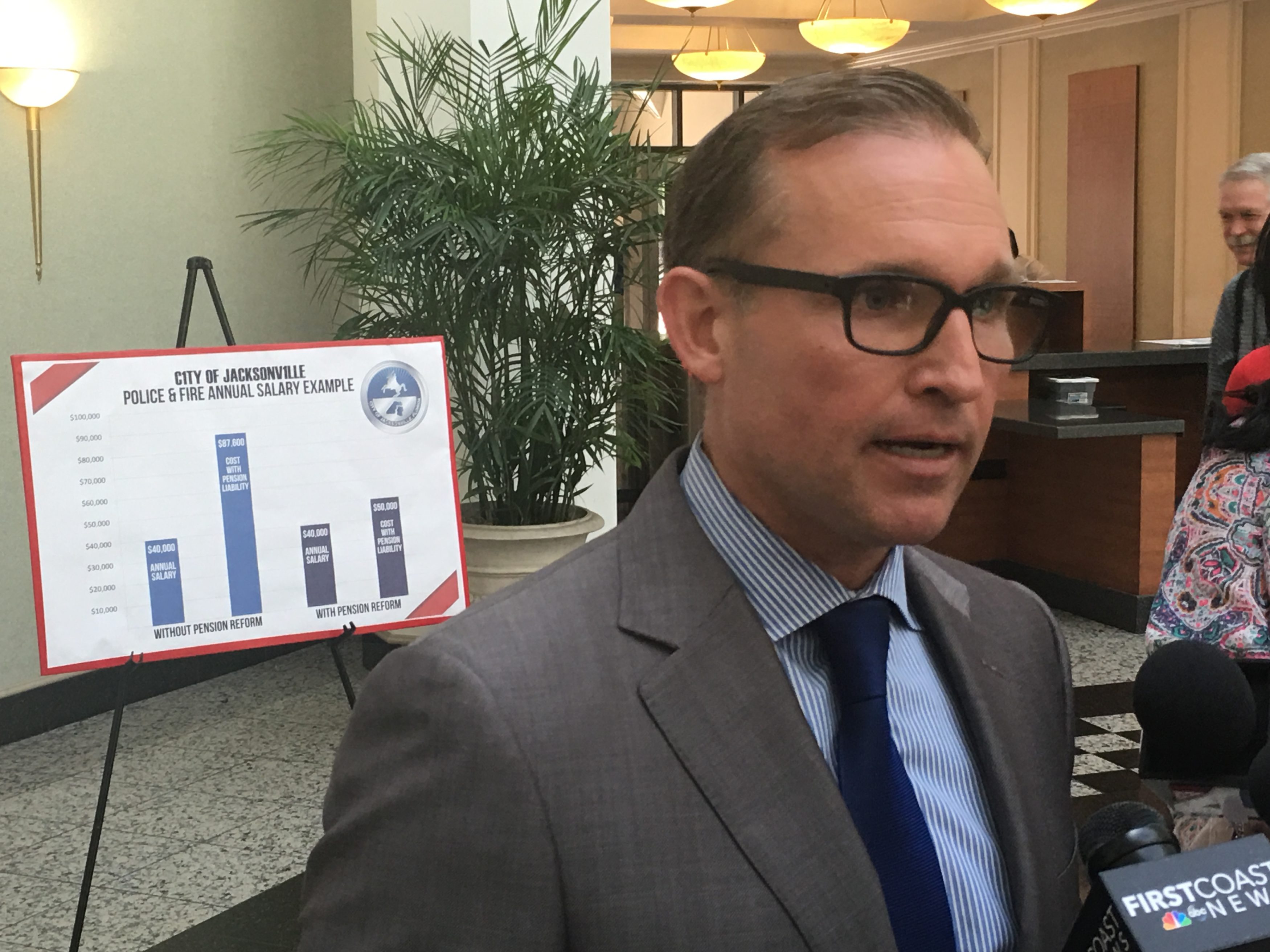

With pension reform closing current pension plans and backing up the repayment with the future assets from a 1/2 cent sales tax, the pension hit in FY 2018 is $218M; if reform fails, the hit is $360M (up from $290M next year).

As CFO Mike Weinstein has said of late, the savings add up to “$1.4B less out of the general fund over the next 15 years,” and “without that revenue” from the half-cent sales tax, the city would have “difficulty matching revenue to expenses.”

So that’s the reality.

—

Three bills ultimately are the most newsworthy.

2017-257 establishes the half-cent sales tax extension. 2017-258 changes pension plans for general employees and correctional workers. And 2017-259 changes plans for police and fire.

The city will offer 25 percent matches for defined contribution plans for police, fire, and correctional workers; for general employees, the match is 12 percent.

The other eleven bills ratified collective bargaining agreements between the city and JEA and various unions.

—